On January 19, 2021, the Greene County Board of County Commissioners were presented the Report on the Financial Statements and Report of Independent Auditor for the Fiscal Year ended June 30, 2020, by April Adams from the Cherry Bekaert accounting firm at their regular scheduled meeting at the Greene County Wellness Center. All units of local government and public authorities in North Carolina are required by North Carolina General Statute 159-34 to have their accounts audited annually and to submit the audit report to the Secretary of the Local Government Commission.

The Cherry Bekaert accounting firm audited the accompanying financial statements of government activities, the business-type activities, the discretely presented component unit, each major fund, and the aggregate remaining fund information for the year ended June 30, 2020, and the related notes to the financial statements, which collectively comprise the County’s basic financial statements for Greene County government.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal controls relevant to the County’s preparation and fair presentation of financial statements to design audit procedures that are appropriate in the circumstances.

Financial highlights mentioned in the report include:

- The assets and deferred outflows of resources of Greene County exceeded its liabilities and deferred inflows of resources at the close of the fiscal year by $41,426,120 (net position).

- The government’s total net position increased by $2,498,466 primarily due to management’s focus on monitoring spending and maximizing revenue collection. This includes a prior period adjustment that increased net position in the business-type activities of $447,882.

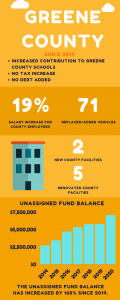

- As of the close of the current fiscal year, Greene County’s governmental funds (which include the general, special revenue, and capital projects funds) reported combined ending fund balances of $12,446,179 after a net decrease in fund balance of $768,275. This compares to combined ending fund balances of $11,677, after a net decrease in fund balance of $324,766 in 2019. Approximately 56.95% of this total amount of $7,091,319 is available for spending at the government’s discretion (unassigned fund balance). In 2019, the unassigned fund balance was $5,884,180 or 50.39% of combined ending fund balances.

- At the end of the fiscal year, the unassigned fund balance for the General Fund was $7,091,319, or 38.33% of total General Fund expenditures for the fiscal year. In 2019, the unassigned fund balance in the General Fund was $5,884,180 or 33.20% of total General Fund expenditures.

- Greene County’s total debt decreased by $1,072,098 or 2.71% during the current fiscal year. No new debt was issued. Principal payments of $1,072,098 were made by the County during the year.

The draft audit presented to the Board of County Commissioners can be viewed below:

https://drive.google.com/file/d/1MMsoI4URFfU28ymwG5oWWFTZpaTn9fdA/view?usp=sharing